x 90px (h)")

x 90px (h)")

x 90px (h)")

![]()

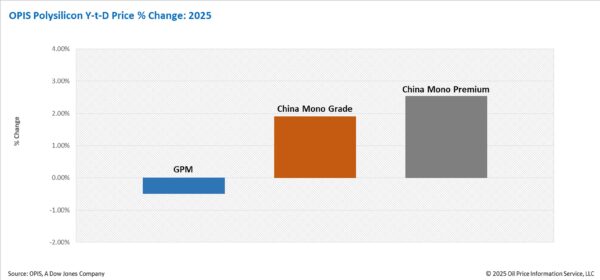

- The Global Polysilicon Marker (GPM), the OPIS benchmark for polysilicon produced outside of China, was assessed at $20.260/kg, or $0.046/W this week.

- The global polysilicon market remains stable, with no significant changes in buying and selling dynamics.

The average operating rate of global polysilicon manufacturing is around 60%, with a total monthly output of approximately 6,000 MT, according to market sources.

However, sales continue to be driven primarily by three to four major wafer manufacturers, who remain willing to place monthly orders under long-term contracts. As monthly consumption falls short of total production, inventory levels are rising on both the supplier and buyer sides. The market is also awaiting the expansion of non-Chinese wafer production capacity to diversify the customer base. Given these conditions, sources indicate that a price increase for global polysilicon in the short term remains unlikely.

A market observer analyzing trade flows noted that wafers made from global polysilicon are primarily sold to Indonesia and Laos, where they are further processed into downstream products for export to the United States. Additionally, a company in Cambodia, set to launch 2 GW of ingot production in May, has emerged as a potential new customer for global polysilicon suppliers, given its estimated annual polysilicon demand of approximately 5,000 mt.

Meanwhile, the planned 100,000-MT-per-year polysilicon plant in Oman is reportedly expected to commence partial production in May or June. However, sources indicate that further delays are possible, as the peak summer season starting in May could pose challenges for energy-intensive manufacturing operations in the region.

The China Mono Grade, OPIS’ assessment for mono-grade polysilicon prices within the country, remained stable this week at CNY 33.625 ($4.63)/kg, equivalent to CNY 0.076/W. Similarly, the China Mono Premium, OPIS’ price assessment for mono-grade polysilicon used in n-type ingot production, held steady at CNY 40.375/kg, or CNY 0.091/W.

Despite a surge in domestic solar installations in China, driven by two new solar policies set to take effect in May and June, wafer manufacturers remain cautious in their polysilicon procurement, thereby limiting the potential for polysilicon price increases. This cautious approach is largely due to the approximately 200,000 MT of polysilicon currently held in wafer plant inventories, which is sufficient to support the production of over 80 GW of modules.

Market sources noted that polysilicon prices face a challenging outlook due to a potential increase in production. A major producer with an annual capacity of approximately 250,000 MT — previously shut down and ranked lower among the top five — is set to resume operations soon, potentially driving up polysilicon output in April. Additionally, a new polysilicon project with an annual capacity of 140,000 MT officially entered the trial production stage in late March, though its impact on supply may not become significant until the third quarter.

End-user demand in China is expected to decline in the third quarter following the implementation of new solar power policies, potentially triggering another round of price softening across the photovoltaic industry chain. Industry insiders have therefore cautioned companies to proactively prepare for these challenges.

Source: OPIS

OPIS, a Dow Jones company, provides energy prices, news, data, and analysis on gasoline, diesel, jet fuel, LPG/NGL, coal, metals, and chemicals, as well as renewable fuels and environmental commodities. It acquired pricing data assets from Singapore Solar Exchange in 2022 and now publishes the OPIS APAC Solar Weekly Report.

This article was originally published in pv magazine and is republished with permission.