x 90px (h)")

x 90px (h)")

x 90px (h)")

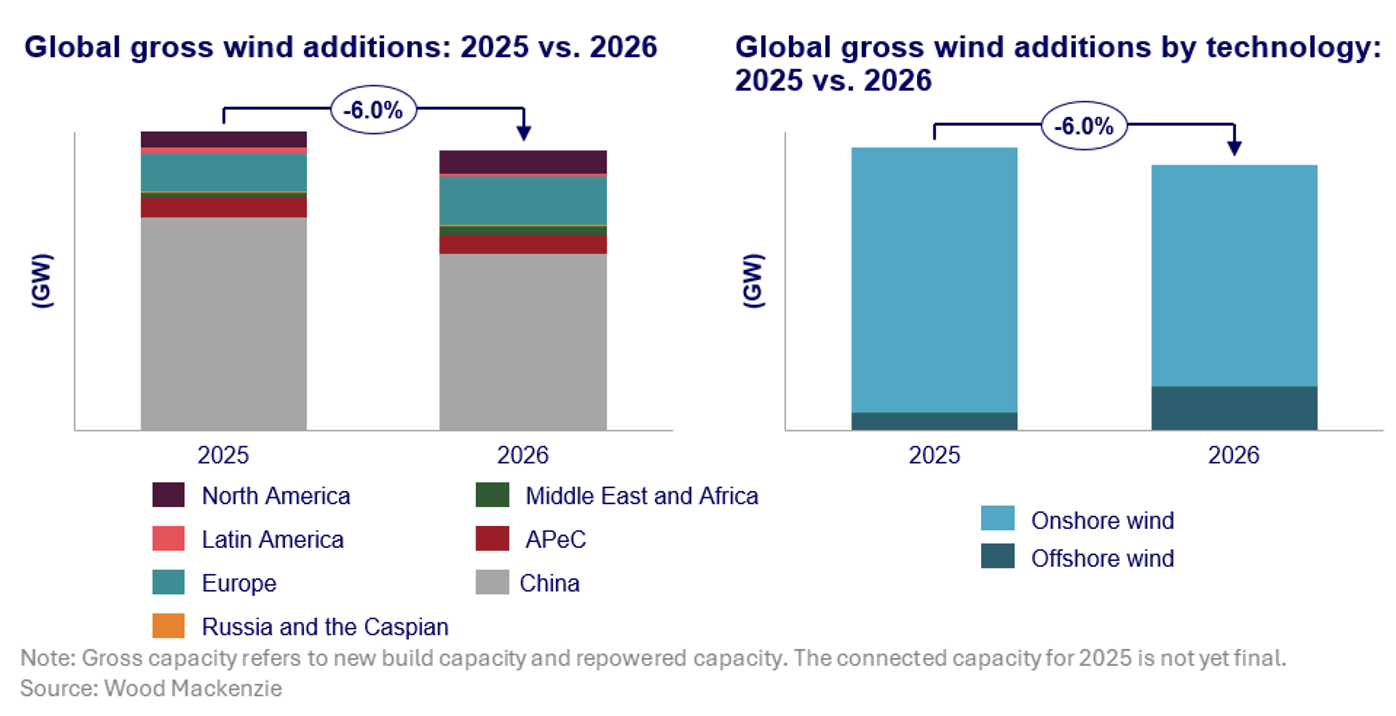

- Global onshore wind installations expected to decline as China slows while Europe and the United States accelerate.

- Offshore wind capacity set to more than double in 2026 as new tender frameworks are tested.

- Wind energy costs begin to stabilise amid ongoing supply chain and ageing asset challenges.

After a record year in 2025, the global wind power sector is entering a more complex phase in 2026, marked by slower installations in China and strong momentum in offshore wind and Western markets. This is according to the latest Wood Mackenzie report, Wind power: What to look for in 2026, released this week.

The research highlights a projected six percent decline in global gross onshore wind installations in 2026 compared to 2025. The slowdown is largely attributed to China, following the conclusion of its 14th Five Year Plan. China has been the dominant force in global wind additions, and its pullback is expected to weigh on overall installation figures.

Outside China, however, the outlook is more positive. Europe is forecast to account for a significant share of global onshore wind additions in 2026, supported by increased permitting and capacity awards in key markets such as Germany. The United States is also expected to deliver strong growth as developers move quickly to secure incentives that are due to expire.

Wood Mackenzie data shows that as of November 2025, 84 percent of forecast wind capacity outside China for 2026 has already reached final investment decision or is under construction, suggesting limited execution risk despite the possibility of some projects slipping into 2027.

Offshore wind is expected to be the standout performer in 2026, with new capacity additions more than doubling year on year. This surge is driven by a pipeline of projects moving forward after several years of tender delays and cancellations.

Governments are now rolling out a new generation of offshore wind tenders designed to better reflect market realities, including higher costs and financing risks. These revised frameworks aim to ensure that projects are not only awarded but also successfully built. The United Kingdom’s upcoming Allocation Round 7 is expected to be an early test of this approach.

Despite the renewed momentum, Wood Mackenzie cautions that timing gaps remain. Offtake cancellations in recent years are expected to create a slowdown in project delivery from 2028, with long development timelines limiting the ability to respond quickly. This could place renewed strain on global supply chains and drive costs higher if not carefully managed.

On the cost front, wind energy capital expenditure trends are beginning to diverge less sharply across regions. In China, onshore turbine prices rebounded in 2025 and are expected to stabilise in 2026, although developers face ongoing revenue pressure. In Western markets, costs remain elevated due to labour shortages, high interest rates, geopolitical uncertainty and policy risk.

While material costs have started to ease, turbine prices continued to rise in 2025 as manufacturers prioritised margin recovery. Wood Mackenzie expects 2025 to mark the peak of cost inflation, with gradual relief emerging from 2026. In Europe, onshore turbine prices are forecast to plateau through to 2027, with only modest declines anticipated.

Another growing issue for the sector is the ageing global wind fleet. A significant portion of installed capacity is now over 20 years old, raising questions around performance degradation, lifetime extensions and decommissioning. Asset owners continue to favour extending operational life, particularly in Europe and North America, where retrofit and partial repowering capabilities are well established.

Decommissioning activity remains limited and has so far failed to keep pace with the increasing volume of ageing assets, leaving end of life management as an unresolved challenge in mature wind markets.

Wood Mackenzie concludes that while the wind industry will continue to face difficult market conditions in 2026, evolving policy frameworks, technology improvements and new commercial strategies are expected to strengthen the sector’s resilience over the medium term.

Link to the full report HERE

Author: Bryan Groenendaal