x 90px (h)")

x 90px (h)")

x 90px (h)")

- Global energy storage cell shipments projected to reach 801 GWh in 2026 while installations rise to 353 GWh.

- Tight cell supply and rising lithium carbonate prices expected to support higher battery prices.

- Emerging markets including Australia, India, Brazil and South Korea gaining momentum in global deployments

The global energy storage market is set to maintain strong growth in 2026 as tightening supply conditions, evolving battery technologies and expanding emerging markets reshape the industry landscape.

According to market intelligence firm InfoLink Consulting, global energy storage cell shipments are expected to reach 801 GWh in 2026. Energy storage system integration shipments are projected at 600 GWh while total installations are forecast to reach 353 GWh. The cell segment continues to dominate supply chain focus as demand outpaces production.

Since the second half of 2025 the market has experienced persistent shortages of energy storage cells. Demand has exceeded supply and this imbalance is expected to continue into 2026. Most new manufacturing capacity is scheduled to come online during the second half of the year which means supply conditions will likely remain tight in the first half before easing moderately later in the year.

Manufacturers are also taking a more cautious approach to expansion compared with previous growth cycles. Lithium battery production requires high capital investment and the reduction of subsidies has encouraged companies to be more conservative with spending. At the same time the industry is transitioning from 314 Ah battery cells to next generation formats above 500 Ah. As a result capacity expansion for the current 314 Ah format has slowed while the larger formats remain in early stages of development.

Technology upgrades are continuing across both utility scale and residential energy storage segments as the market moves toward larger capacity battery cells.

In the utility scale segment cell capacities are shifting from 314 Ah toward larger formats including 587 Ah and 588 Ah. Procurement frameworks issued by Chinese state owned enterprises in early 2026 continue to specify a minimum requirement of 314 Ah which indicates the format remains widely used while acceptance of larger cells continues to grow.

Following the mass production of 587 Ah cells by leading manufacturers in the second half of 2025, second tier suppliers are expected to begin large scale production of high capacity cells from the second quarter of 2026. InfoLink estimates that battery cells above 500 Ah could account for nearly 15% of the utility scale storage market in 2026.

The residential energy storage market is also shifting to larger formats. Before 2025 the segment was dominated by 100 Ah cells with smaller formats such as 50 Ah and 72 Ah supplementing supply. Rapid growth in residential storage demand through 2025 however tightened supply and pushed prices for 100 Ah cells sharply higher.

The price gap between 100 Ah cells and larger 280 Ah and 314 Ah formats has widened to more than RMB 0.5 per Wh. This has accelerated interest in the larger cells which are expected to reach around 20% market penetration in residential storage applications in 2026.

Lithium carbonate prices have also entered a period of strong volatility. Prices strengthened from the fourth quarter of 2025 due to concentrated demand, temporary supply disruptions and improving market sentiment. Spot prices in early 2026 briefly exceeded RMB 180,000 per metric ton before entering a period of fluctuations at elevated levels.

The pricing mechanism for lithium carbonate has evolved from being driven mainly by supply and demand fundamentals to a model increasingly influenced by market expectations and sentiment.

Supply expansion continues across the lithium salt industry with new capacity expected to grow more than 20% year on year in 2026. Much of this expansion is concentrated in China and Africa while the share of recycled lithium feedstock is also increasing.

Demand remains resilient. While growth in new energy vehicles may slow slightly, power battery demand is expected to remain stable. Meanwhile the energy storage sector continues to show strong expansion supported by policy incentives and the rapid development of overseas markets.

Overall both supply and demand for lithium carbonate are expected to increase during 2026, easing the structural oversupply that emerged in 2025. Prices are forecast to fluctuate between RMB 100,000 and RMB 190,000 per metric ton with the annual average likely between RMB 120,000 and RMB 160,000 per metric ton.

The lowest price levels are expected from late second quarter through the third quarter before strengthening again in the fourth quarter.

Energy storage cell prices have already risen sharply. Strong demand since the fourth quarter of 2025 has pushed the market from oversupply into shortage while rising raw material costs have increased production expenses. Cell costs in January 2026 were more than 23% higher than in October 2025 while transaction prices for mainstream 314 Ah cells increased by more than 16%.

For the remainder of 2026 mainstream cell prices are expected to remain above RMB 0.300 per Wh with average levels more than 15% higher than in 2025.

In contrast the energy storage system integration segment is under greater pricing pressure. System integrators face rising cell costs while competition continues to intensify. Bid prices for integration projects in China have increased by less than 10% since the fourth quarter of 2025.

As large capacity cells become more widely adopted and integrated system products deliver cost reductions, integration prices in China are expected to remain flat or decline slightly compared with 2025. In overseas markets however higher entry barriers and changes to export rebate policies may support higher system prices in some regions.

Image credit: Infolink Consulting

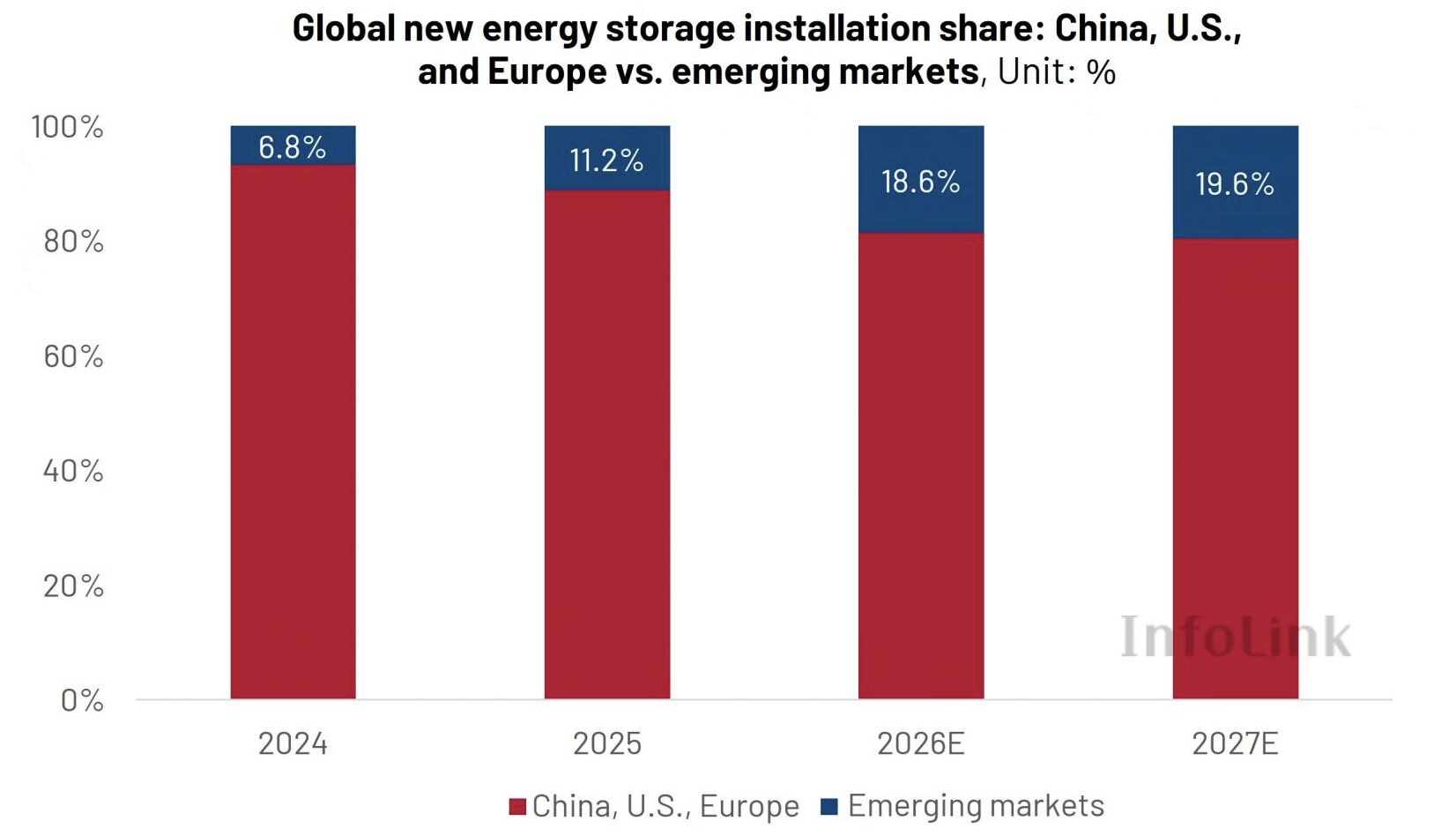

While China, the United States and Europe remain the dominant drivers of global energy storage demand, emerging markets are expected to become increasingly important growth engines.

The share of global installations from emerging markets could approach 20% in 2026. Among these markets, Australia, India, Brazil and South Korea are attracting increasing attention from energy storage manufacturers.

Australia is already showing strong momentum. The country added 11.4 GWh of new energy storage capacity in 2025 which represented a 338% increase compared with 2024 and made it the third largest market globally after China and the United States. Installations are expected to rise further to around 13 GWh in 2026.

Market growth in Australia is being driven by stronger policy support, including projects awarded under the Capacity Investment Scheme that are expected to begin operations from 2026. A residential subsidy program worth AUD 7.2 billion is also supporting demand. In addition the accelerated retirement of coal fired power plants is increasing structural demand for storage as the electricity system transitions toward renewable energy.

Other emerging markets are also building momentum.

In India government policies including mandatory storage requirements and Viability Gap Funding subsidies are supporting deployment. Large scale tenders launched by the Solar Energy Corporation of India and NTPC Limited during 2024 and 2025 are entering delivery phases which is expected to drive a significant increase in installations during 2026.

Brazil has also taken steps to establish a market framework. New legislation introduced in November 2025 formally recognized energy storage as an independent activity while introducing tariff and tax incentives. The country plans to hold its first battery energy storage capacity auction in April 2026.

South Korea is strengthening its utility scale pipeline as well. The country announced results of its second round 3.24 GWh storage tender in February 2026 bringing the combined capacity tendered over the past two years to around 6.5 GWh.

Although construction timelines mean that projects in Brazil and South Korea may not translate into large installation volumes in 2026, the policy and procurement developments are laying the foundation for future growth.

Across the global energy storage sector, the return of tight supply conditions, rising battery prices, technology upgrades and accelerating emerging markets reflect a broader repricing and restructuring cycle across the supply chain. In this environment manufacturers that can balance capacity expansion, technology development and international market growth are likely to gain a competitive advantage as the industry continues to evolve.

Author: Bryan Groenendaal