x 90px (h)")

x 90px (h)")

x 90px (h)")

- Rho Motion reports that energy storage installations surpassed expectations in 2024, with over 200GWh of capacity installed worldwide.

- This marks yet another record year for the industry growing 53% year on year.

- The majority of this growth was driven by utility scale installations, primarily in China.

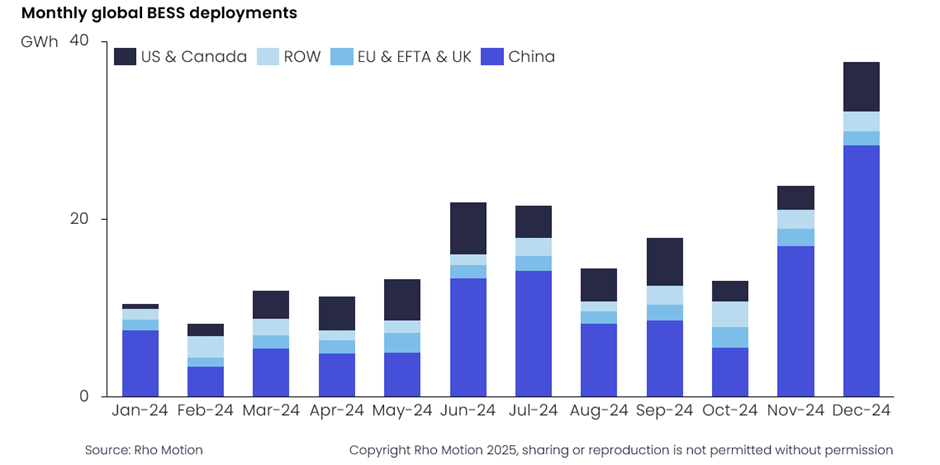

Grid scale installations see the strongest growth

Pete Tillotson, Senior BESS analyst at Rho Motion commented, “Once again China led the way with new deployments in 2024, accounting for over 108GWh of new grid-scale capacity, and 66% year on year growth. Across the total market China’s capacity accounted for 59% of total BESS deployed.”

Europe and North America also saw strong growth in grid scale installations growing 110% and 66% respectively. Historically growth in Europe has been small, however in 2024, new markets showed signs of opening up boosting deployments in the country.

Growth in North America remained heavily localised with California alone accounting for half of the total 40GWh installed in the region.

China cheapest

Iola Hughes, head of Research at Rho Motion, notes that BESS system prices have fallen below $100/kWh for the first time in China on the back of record low LFP cell price. Despite this, system prices outside of China, although declining, can typically cost more than twice that. “In the recent release of the Rho Motion Q4 BESS Quarterly Outlook, we considered the cost saving scenario that has resulted in this significant differential. The Tesla Megapack, a premium product, is currently available to order at ~$240/kWh for a 2-hour system. Meanwhile the average BESS system price in China fell to $82/kWh in Q3 2024 based on reported contracts, more than halving over the last two years!”

Hughes adds that cost savings are being made on a number of metrics from reduced margins to vertical integration and low OPEX. “Whilst Tesla reported a record margin of 30% for its energy storage business in its Q3 financials, reports of zero to negative margins are present in China under the super competitive ‘price-war’ environment. How much further these prices can fall is the big question – in China we could be approaching a floor, while outside of China things could continue to decline someway as competition grows,” said Hughes.

The behind the meter market remains in growth, but with some caveats

Behind the meter markets, both commercial & industrial (C&I) and uninterrupted power supply (UPS), grew 15% globally, with 40GWh installed. These markets remained spread globally with China and Europe accounting for just under 30% of the total market respectively, and North America accounting for 15%.

However, in Europe growth in this market showed signs of stagnation. Historically, subsidies supported strong growth in Europe’s market, but a combination of stable electricity pricing and reduced subsidies has led to this slowdown in growth.

LFP remained dominant in the market

LFP’s dominance grew throughout 2024 accounting for 87% of total energy storage installations, up from 83% in 2023. However, other technologies such as flow batteries and sodium-based systems also grew in deployments.

- Flow battery deployments grew over 320% compared to 2023 with 2.4GWh of deployments

- Sodium-ion deployments grew 85% compared to 2023, however at a smaller scale with just over 300MWh of batteries deployed.

Head of Research at Rho Motion, Iola Hughes commented, “Low LFP prices remain a barrier to sodium-ion uptake, however several product launches planned for 2025 will likely result in a stronger year.”

The year ahead

The global storage market remains in the early stages of development, excluding a few select markets. After strong growth in 2023 and 2024 this trend is expected to continue into 2025, with new and existing countries developing strong pipelines for the year. In Rho Motion’s pipeline for the 2025 there are over 400GWh worth of planned BESS deployments, however due to cancellations and delays not all of these projects will reach completion.

Author: Bryan Groenendaal

Source: Rho Motion