x 90px (h)")

x 90px (h)")

x 90px (h)")

- The global wind market is projected to expand in 2025, led by China, but the industry still faces headwinds, particularly in the offshore sector, according to Wood Mackenzie.

Wood Mackenzie recently released “What to look for in 2025” reports for both global onshore and offshore wind. Key themes to watch for include: wind policy shifts in the US, a record year of exports for Chinese OEMs and offshore wind tenders, new trade barriers and new markets for offshore opportunities, among others.

Overall, global gross onshore wind installations, including new builds and repowering, are expected to grow by 20% in 2025, according to the report. This surge is mainly attributable to China and the delayed execution of projects in the rest of the world from 2022 and 2023 rather than an uptick in new orders or increased commercial activity outside of China.

For the offshore market, new-build capacity connected in 2025 outside China will be on par with 2024 and stay below 6 GW, followed by a doubling in 2026. The picture is different in China, with connections set to more than double to 12 GW in 2025 following a three-year slump in a pursuit to meet targets for the 14th Five-Year Plan.

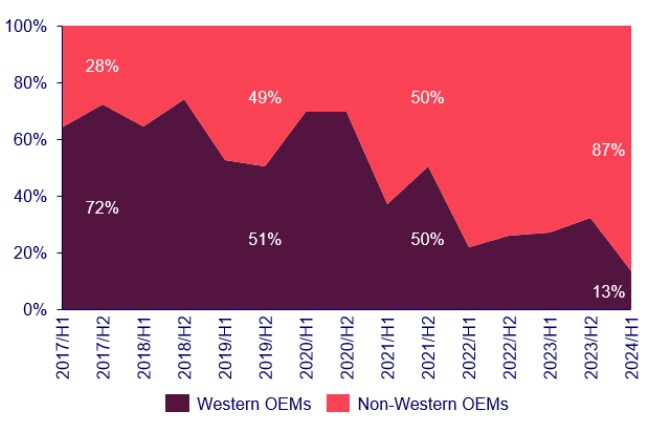

Onshore – Chinese OEMs aim for a record year of exports

According to the report, China accounts for 68% of the global wind turbine manufacturing capacity, undermining Western OEMs’ attempts to foster closer supply chain ties with Chinese suppliers. Wood Mackenzie expects Chinese OEMs to grab an average of 20% of onshore wind share outside of China in the next decade. For 2025 specifically, our OEM market share forecast estimates that 68% of the global grid-connected volume will be from Chinese OEMs.

“Chinese wind OEMs are particularly focused on emerging markets, incentivised by the Belt and Road Initiative and gigawatt-scale green hydrogen projects,” said Leila Garcia Da Fonseca, research director at Wood Mackenzie. “Their strength derives from the massive scale of the Chinese market and supply chain, lower prices, expertise in power system integration and the vacuum that Western OEMs left as they prioritised core Western markets.”

Western OEMs’ share of global order intake, H1 2017 – 2024

Source: Wood Mackenzie Global wind turbine order analysis: Q3 2024

Onshore – Repowering and decommissioning of installed assets will increase year-on-year

An ageing fleet globally will attract investment in repowering and decommissioning activities in 2025, reaching 4.6 GW and 4.3 GW, respectively, according to Wood Mackenzie.

Nearly 11 GW of onshore wind capacity will reach 20 years of operations by 2025, bringing the global cumulative volume of turbines with 20+ years of operational life to 48 GW in total. China will account for 56% of the estimated repowering capacity and 60% of the decommissioning volume in 2025.

“Outside of China, governments in leading onshore wind markets with ageing fleets will have to provide asset owners and developers with more support and incentives to replace older turbines,” said Garcia Da Fonseca. “Persistent high re-development prices, low maintenance costs in some markets, and high dismantling and disposal expenses continue to discourage asset owners from repowering.”

Offshore – Components will travel further and encounter more trade barriers

In 2024 the Chinese supply chain pushed to penetrate more offshore wind segments, most notably turbines, monopiles, installation vessels and blades. These trends will be sustained in 2025. In addition, new markets will start to install offshore wind turbines, and the supply chain will globalise. As a result, Wood Mackenzie forecasts components will start travelling further from 2026, making transport an increasingly important parameter in contract negotiations in 2025.

At the same time, the number of trade-limiting initiatives has increased, and with the recent election in the US and the situation in Europe, there is little to suggest that the rollout of trade-limiting initiatives will slow down in 2025.

“Due to the globalised nature of the offshore wind supply chain, tariffs would, all else being equal, have an impact on offshore wind costs,” said Finlay Clark, principal research analyst, global offshore wind for Wood Mackenzie. “In 2024, new initiatives were launched to support the European supply chain. We expect this to remain on the table for 2025. However, an increase in demand is also needed to maximise the impact of these policies.”

Offshore – Will new markets be more attractive than the established markets in 2025?

At the end of 2024, the Danish offshore wind tender in the North Sea failed to attract any bidders. However, 72% of the tenders for bottom-fixed offshore wind in the North Sea were only oversubscribed by a factor of two or less. At the same time, tenders in new markets and for floating wind have been able to sustain the rate of oversubscription and even, in some cases, increase the rate of oversubscription. The cost pressures in the new markets are not less.

“In most new markets, depending on the technology, protectionist policies, area characteristics and proximity to the supply chain it is mainly greater,” said Søren Lassen, head of offshore wind research for Wood Mackenzie. “Instead, the main driver behind the steeper decline in the rate of subscription in the established markets is that policymakers are focusing more on how to squeeze the bidders while the new markets are still offering subsidies to help establish the market.”

The downward trend in tender subscriptions for established markets and the flat rate of tender subscription in new markets shows the outsized role that tender frameworks play for offshore wind. As such, Wood Mackenzie expects to see changes in tender frameworks in 2025. Some are already announced – this includes the three core markets in APeC and the UK.

In tandem with this, a new wave of markets is advancing their route-to-markets across the Baltic Sea, Southern Europe and Asia will be looking to leverage the hard-thought learnings of the tenders.

Other trends covered the reports are: the impact of new technology, factories and vessels and their impact on execution for offshore wind, unparalleled M&A opportunities and the continued recovery of the onshore wind market.

Read the onshore and offshore reports report here.

Author: Bryan Groenendaal