x 90px (h)")

x 90px (h)")

x 90px (h)")

- With up to US$185 billion of investment committed to developing 27 billion barrels of equivalent (boe), upstream oil and gas financial investment decisions (FID) will likely increase this year, according to a new analysis from Wood Mackenzie. A barrel of oil equivalent (BOE) is a term used to summarize the amount of energy that is equivalent to the amount of energy found in a barrel of crude oil.

“Achieving FID on oil and gas projects is harder than it used to be, but with fewer sanctioned in 2022 than was expected, we believe we will see a slight uptick in activity this year, with over 30 of the 40 most viable projects likely to reach this milestone,” said Fraser McKay, vice president, Head of Upstream Analysis for Wood Mackenzie. “Most operators will remain disciplined and carbon mitigation will remain a key part of many FID projects.”

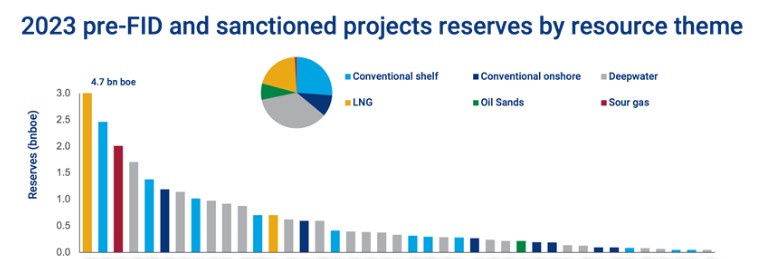

NOCs will dominate project sanctions in 2023

National oil companies (NOCs) will control the largest investment opportunities this year, taking advantage of huge, discovered resources, while boasting the lowest unit costs. The average unit development cost of US$7/boe in 2023 is down slightly from 2022.

“International oil companies (IOCs) will be focusing largely on higher-cost but higher-return deepwater developments,” said McKay. “All will be acutely aware of how oil and gas project sanctions are playing out in the public domain and the scrutiny to which their associated emissions will be subject.”

Robust economics and carbon mitigation will be key for most projects

In 2023 projects will require an average of US$49/barrel of crude (bbl) to generate a breakeven 15% internal rate of return (IRR). However, a weighted average IRR of 19%, at US$60/bbl, would be the lowest level since 2018. Rapid paybacks will be a key economic indicator as well, with the average for this year’s projects at nine years.

“Short-cycle and small-scale offshore projects will outperform in terms of both paybacks and returns,” said Greg Roddick, Principal Analyst of Upstream Research. “Long-life liquified natural gas (LNG) projects are compromised when it comes to IRRs, but their attractive and stable future cash flows will be strategically important.”

The class of 2023 emissions intensity of 19 kgCO2 boe is only just below the global onstream average of 22 kgCO2 boe, but similar to that of the Class of 2022.

“Advantaged deepwater oil and shelf projects will outperform on emissions, but LNG, sour gas and some onshore projects require mitigation measures,” added Roddick.

Author: Bryan Groenendaal

Source: Woodmac