x 90px (h)")

x 90px (h)")

x 90px (h)")

- Wood Mackenzie names JA Solar with a score of 91.7 and Trina Solar (91.6) as the top leaders in first half 2025 solar panel (module) rankings.

- The global top ten manufacturers record combined net losses of 2.2 billion dollars amid price pressure.

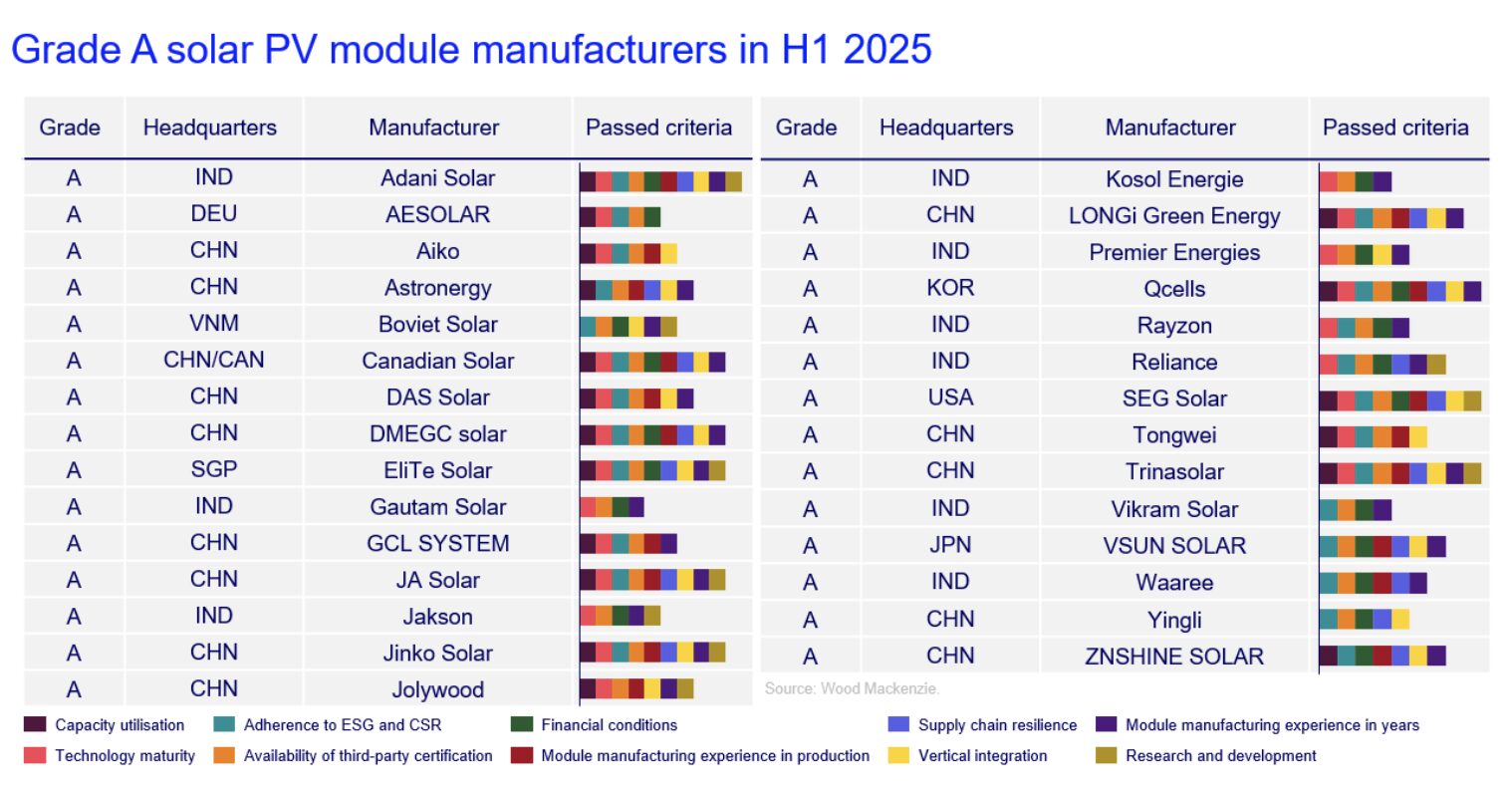

- The new Grade A classification highlights bankable and operationally strong suppliers.

JA Solar and Trinasolar have jointly secured the top position in Wood Mackenzie’s Global Solar Module Manufacturer Ranking for the first half of 2025, underscoring both resilience and rising fragmentation within the global solar manufacturing sector.

The ranking assessed 38 established module manufacturers from nine countries, representing 62 percent of global production capacity and 75 percent of shipments by the first half of 2025. Wood Mackenzie’s methodology combines quantitative scoring with buyer focused criteria based on procurement and bankability requirements.

The ranking reveals a widening operational and financial gap between leading producers and the rest of the market, as oversupply and falling prices continue to weigh heavily on the industry.

According to Wood Mackenzie, the world’s top ten solar module manufacturers accounted for 62 percent of global shipments during the first half of 2025. Despite this dominant position, these companies collectively reported net losses of 2.2 billion dollars over the same period.

Yana Hryshko, Head of Global Solar Supply Chain at Wood Mackenzie, said the results reflect the severity of current market conditions. She noted that even the largest manufacturers are under pressure from sharp price declines, while non Chinese companies in the top ten remained profitable by focusing on premium and protected markets. Financial discipline and operational excellence, she said, are increasingly the key differentiators.

Image credit: Woodmac

The ranking highlights strong performance among leading manufacturers in several areas. The top ten maintained an average utilisation rate of 70 percent in the first half of the year, compared with a global average of 43 percent for other producers. Adani Solar and DMEGC Solar stood out by operating at full capacity. Collectively, the top ten shipped 224 gigawatts of modules, reinforcing a high level of market concentration.

At the same time, Wood Mackenzie points to growing geographic diversification. Manufacturers from India, South Korea, Singapore and the United States are gaining ground, driven in part by tightening trade policies and the search for more resilient supply chains.

A key development in the latest ranking is the introduction of the Grade A classification. This new benchmark is designed to signal operational excellence and bankability, moving the focus beyond shipment volumes to include global procurement standards and risk management. In the first half of 2025, 29 manufacturers across nine countries achieved Grade A status.

Looking ahead, Wood Mackenzie expects the period from 2026 to 2027 to be shaped by consolidation, deeper vertical integration and increased regionalisation of manufacturing. Control across the wafer to module value chain is emerging as a new competitive frontier, with several leading manufacturers expanding into the Middle East and North Africa to create tariff resilient production bases.

Technological advances are also set to accelerate change. Efficiency improvements driven by TOPCon and back contact technologies are expected to push mainstream module performance beyond 25 percent, hastening the phase out of lower grade production lines.

As weaker suppliers exit the market through shutdowns or mergers, leading manufacturers are likely to sustain utilisation rates of between 60 and 75 percent. With global demand forecast to strengthen and pricing expected to stabilise from 2026, the industry is projected to shift from survival mode to strategic investment, with Grade A manufacturers best positioned to benefit from the next growth cycle.

For enquiries on the African continent, email: africa@jasolar.com

Author: Bryan Groenendaal