x 90px (h)")

x 90px (h)")

x 90px (h)")

- As the dust settles following the passage of the USA Inflation Reduction Act (IRA), the electricity industry is only beginning to understand its true impacts.

- One of those impacts is the continued erosion of the business case for new fossil gas power plants.

Over the past decade, fossil gas power plants became the default resource option for utility investment, making up a majority of capacity additions. While over the past few years the total capacity of plants built has declined and high profile cancellations have increased, the USA IRA’s tax incentive provisions will accelerate deployment of cleaner, cheaper electricity — making gas an even less competitive choice.

New RMI analysis shows just how much the IRA changes the game.

The Analysis

We used our Clean Energy Portfolios Model — updated to include resource cost projections that reflect post-IRA levels of tax credits — to identify the lowest cost portfolio of wind, solar, battery energy storage, energy efficiency, and demand flexibility that can provide the same estimated services as a proposed fossil gas plant.

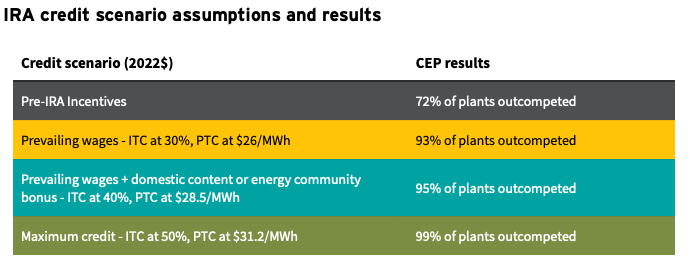

When we ran 76 GW of fossil gas plants proposed before 2035 through our Clean Energy Portfolios Model, we found that the vast majority of plants were more expensive than their respective clean energy portfolios (CEPs), shown in Exhibit 1. In a scenario where clean energy resources use the 30 percent Investment Tax Credit or the Production Tax Credit at $26/MWh, clean energy outcompetes 93 percent of proposed fossil gas plants — more than 20 percent more than pre-IRA.

With additional bonuses for investment in energy communities, use of domestically sourced resources, or siting in low-income communities, in nearly every instance, clean energy beats gas on cost alone. That means that when taking full advantage of the tax credits in the IRA, clean, renewable sources will be cheaper than 99 percent of proposed gas plants — plants that are contributing to price volatility in American household energy bills.

When taking full advantage of the tax credits in the Inflation Reduction Act, clean, renewable sources will be cheaper than 99 percent of proposed gas plants.

The Power of Financial Incentives

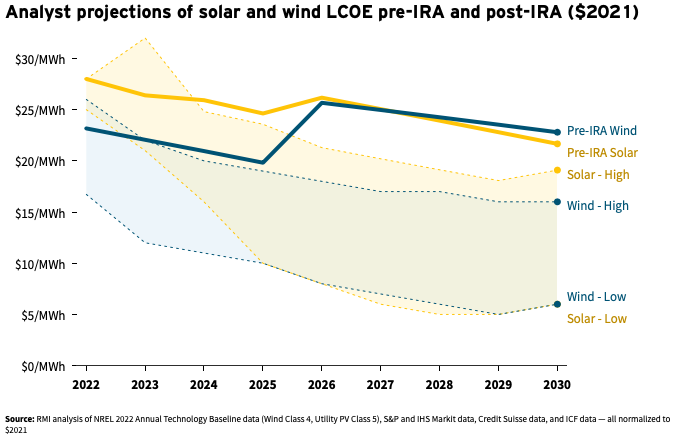

One of the main reasons for this is that post-IRA solar and wind costs are expected to plummet. Analysts are projecting that renewables costs will continue to fall — with jaw-droppingly low prices for wind and solar by the end of the decade.

Credit Suisse, for example, made headlines when it projected $5/MWh wind and solar by 2029. S&P Global and IHS Markit projected numbers nearly as low — with about $10/MWh solar in 2030 falling to $5/MWh by 2035. Consulting firm ICF’s projections, though slightly less bullish, still predict that a levelized cost of energy for solar and wind in 2030 will be 20–35 percent and 38–49 percent lower, respectively, than pre-IRA.

In most of these forecasts, renewable costs fall below the go-forward cost of a combined cycle gas plant — generally expected to be at least $30–$40/MWh. This means it will be cheaper on a per megawatt hour basis to build new wind and solar than to continue to operate existing gas.

Exhibit 3 aggregates these projections (Credit Suisse, S&P Global and IHS Markit, and ICF’s low projections for 2030) into charts that show an indicative range of levelized cost of energy for wind and solar post-IRA, compared with NREL’s 2022 Annual Technology Baseline pre-IRA.

While our analysis in the Clean Energy Portfolios Model only looked at battery energy storage and demand flexibility to provide firm, dispatchable energy, a host of new resource options may also be cost-competitive with fossil gas by the end of the decade. A range of “clean firm” technologies will increasingly compete directly with fossil gas, such as alternative energy storage technologies, geothermal, advanced nuclear, hydrogen-fired turbines, and carbon capture and storage.

Updated Resource Plans and Procurement Processes Can Unlock $5 Billion per Year in Savings

RMI’s analysis and other independent analysts are showing that the IRA can fundamentally change the math on the next right utility investment — and deliver substantial savings to customers. These aren’t far-off future projections either. Cheaper, cleaner energy is the result of strong policy we passed this year.

There are actions regulators and utilities can take today to realize the IRA’s projected $5 billion per year in savings for their ratepayers. New resource plans can include updated resource costs that accurately represent the new tax credits, seek to represent the full range of resources that may be commercially available within the planning horizon, and demonstrate how they will use additional IRA funding sources such as the Energy Infrastructure Reinvestment program. While costs remain uncertain, regulators and utilities can use all-source procurement — a competitive process that solicits bids from all types of resources — for near-term needs to discover the market prices and relative competitiveness across resources.

As these changes begin to make their way into utility planning and procurement, we’re starting to see results:

- DTE Energy in Michigan filed its Integrated Resource Plan in early November, with a scenario that factored in IRA tax incentives. Utility executives reported that they expected the IRA to lower the price tag of their 20-year plan for customers about $500 million.

- The Minnesota Public Utilities Commission approved Xcel’s request this week to build 460 MW of solar at a retiring coal plant site — part of a CEP that will avoid a new gas plant. Xcel reported that the IRA was anticipated to save ratepayers 30 percent over its initial estimate of project costs.

- Duke Energy in Florida is providing customers with a $56 million refund as a result of solar tax credits.

- Ameren is proposing to lower customer rates by 4.5 percent.

To fully realize the benefits of the IRA, now is the time for utilities and regulators to reevaluate plans for investing in new fossil gas power plants and take advantage of the opportunity to deliver ratepayer savings with cleaner options.

Author: Lauren Shwisberg

This article was originally published by the Rocky Mountain Institute and is republished with permission.

Disclaimer: The articles expressed in this publication are those of the authors. They do not purport to reflect the opinions or views of Green Building Africa or our staff. The designations employed in this publication and the presentation of material therein do not imply the expression of any opinion whatsoever on the part Green Building Africa concerning the legal status of any country, area or territory or of its authorities.