x 90px (h)")

x 90px (h)")

x 90px (h)")

- Global energy storage system shipments reach 421.16 GWh in 2025, up 75.48% YoY.

- Utility scale segment dominates with 375.25 GWh shipped and CR10 at 60.64%.

- Cross sector entrants and global manufacturing strategies raise competitive pressure ahead of 600 GWh forecast for 2026.

InfoLink Consulting has released its 2025 global energy storage system shipment rankings, drawing on its proprietary energy storage supply chain database, confirming another year of accelerated expansion across the sector.

In 2025, global ESS shipments reached 421.16 GWh, marking a 75.48% YoY increase. Demand was released simultaneously across multiple application scenarios, with regional markets demonstrating synchronized growth momentum throughout the year.

A clear tiered structure emerged within the ESS integration segment. The top five suppliers by shipment volume were Tesla, Sungrow, BYD, Huawei and CRRC Zhuzhou Institute. Over the course of the year, the top three suppliers remained in close contention, alternating in the leading position with only marginal differences in market share.

The top ten manufacturers broadly formed a three tier structure at approximately 40 GWh, 20 GWh and 10 GWh. The 10 GWh tier corresponds largely to the eighth to twelfth ranked companies, where shipment gaps remain narrow and positions shift almost quarterly. Further reshuffling within the top ten is expected in 2026.

Globalisation has become a defining theme. United States based players such as Fluence are establishing integration facilities in Asia, while Chinese leaders including Sungrow are expanding integrated capacity across the EMEA region. Against a backdrop of complex geopolitical dynamics, reliance on a single manufacturing hub is increasingly viewed as a structural risk. Multi location deployment strategies are emerging as a means to enhance resilience to regional policy shifts while capturing localised demand growth.

Cross sector expansion is also accelerating. Wind and solar developers are moving vertically to deliver integrated wind solar storage solutions, while leading lithium battery manufacturers are leveraging scale advantages to expand downstream into system integration. Traditional industrial players are pursuing diversification strategies in search of new growth avenues. As major entrants bring technological, financial and channel strength into the integration segment, competitive intensity is expected to increase further.

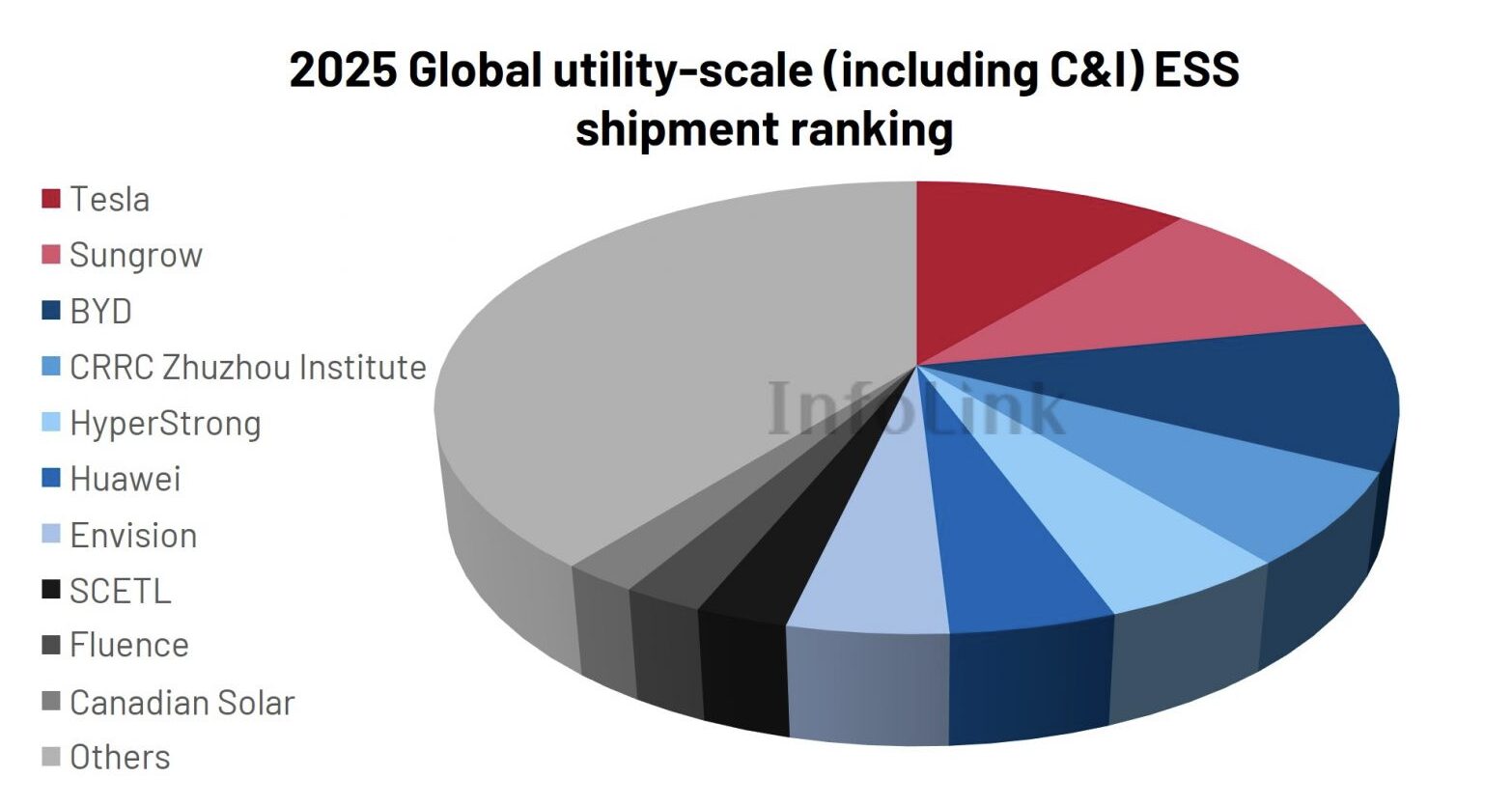

The utility scale segment continues to anchor global demand. In 2025, utility scale ESS shipments reached 375.25 GWh, up 77.84% YoY. The CR10 stood at 60.64%, reflecting a medium to high level of market concentration. While leading players are consolidating scale advantages, competitive dynamics remain fluid.

Source: InfoLink’s Global Energy Storage Supply Chain Database

The top five utility scale suppliers were Tesla, Sungrow, BYD, CRRC Zhuzhou Institute and HyperStrong. Although rankings have remained relatively stable in recent quarters, the market landscape is not yet fully consolidated. Vertical integration progress among midstream players and the strategic repositioning of cross sector entrants warrant close monitoring.

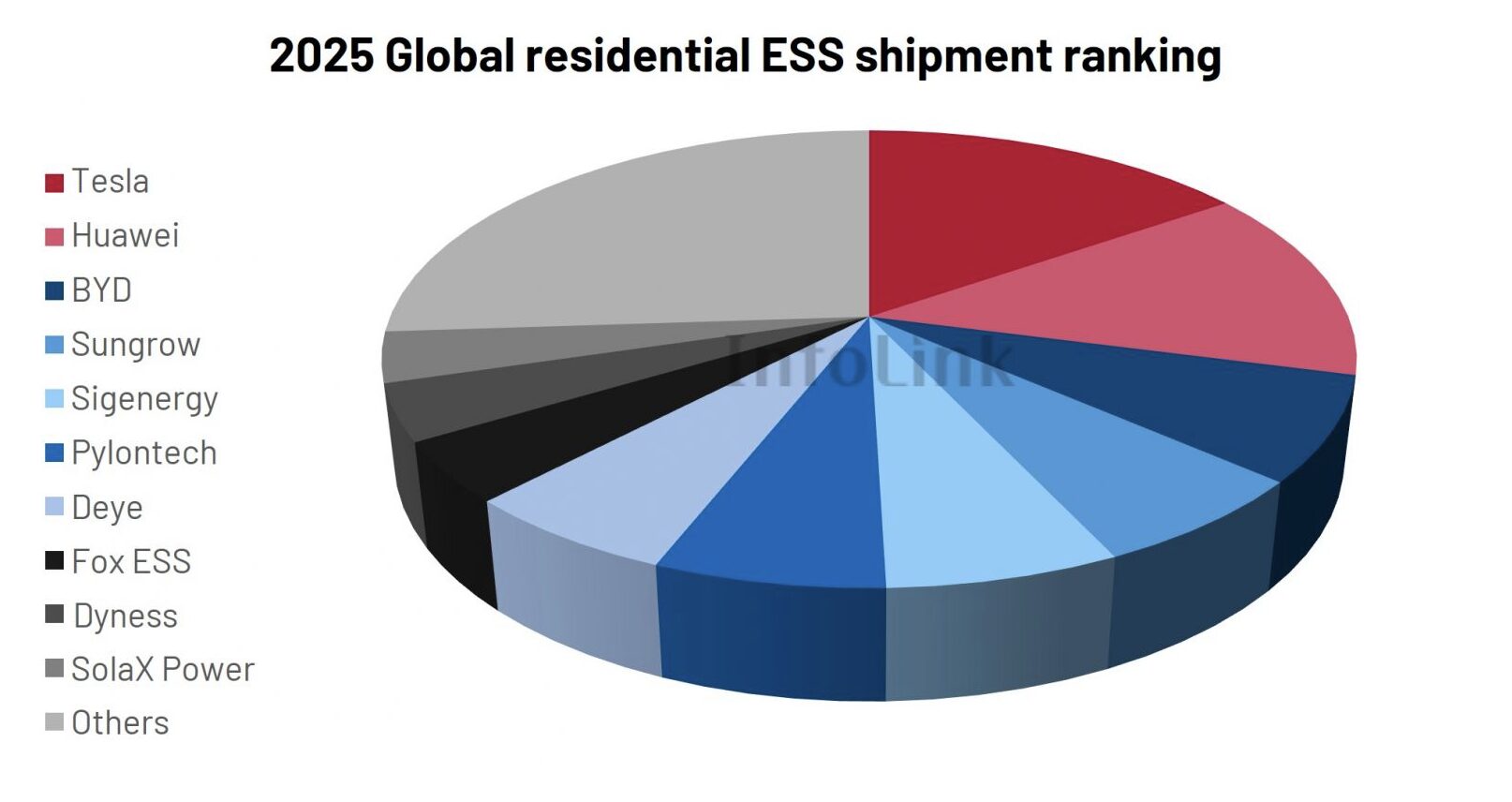

In the residential segment, global ESS shipments reached 35.11 GWh in 2025, up 75.55% YoY. Although fourth quarter shipments declined quarter on quarter, overall volumes remained at elevated levels.

Source: InfoLink’s Global Energy Storage Supply Chain Database

The top five residential suppliers were Tesla, Huawei, BYD, Sungrow and Sigenergy. Among the top ten players, shipment volumes were segmented into three broad tiers of 1 to 2 GWh, 2 to 3 GWh and above 4 GWh.

With new stimulus policies rolling out across several European markets, a regional recovery is anticipated in 2026. Suppliers with strong local market positioning may leverage this rebound to reshape competitive dynamics.

Based on current project pipelines and manufacturer shipment targets, InfoLink maintains its forecast of 600 GWh in global ESS system shipments for 2026, with robust growth expected to continue.

However, strong demand growth does not fully offset underlying structural imbalances in the supply chain. As a new round of price increases unfolds, integrators that fail to align cost control with effective price pass through mechanisms risk revenue growth without corresponding margin expansion. This margin pressure is emerging as a critical determinant of long term competitiveness in the global ESS sector.

The shipment volumes and rankings presented are based on regular interviews with upstream and downstream industry participants, supplemented by market research estimates where direct data was not provided. In cases of discrepancy, manufacturers’ official disclosures prevail.

Author: Bryan Groenendaal