x 90px (h)")

x 90px (h)")

x 90px (h)")

- Global energy storage cell shipments rose nearly 95 percent year on year in 2025, reaching 612.39 GWh.

- Market concentration eased slightly as second, and third tier suppliers gained momentum.

- Utility scale storage remained the main growth driver, while non-China markets accounted for more than half of shipments in the second half of the year.

Global energy storage cell shipments reached 612.39 GWh in full year 2025, representing year on year growth of 94.59 percent, according to the latest Global Energy Storage Supply Chain Database released by InfoLink Consulting. Quarterly shipments increased steadily through the year, with fourth quarter volumes exceeding 200 GWh for the first time.

InfoLink notes that the global market experienced a notable reshuffle in supply and demand dynamics during 2025. Industry concentration among the top ten suppliers stood at 88.8 percent, remaining below 90 percent for two consecutive quarters. This trend points to strengthening shipment momentum among second and third tier manufacturers, with growth broadening beyond the leading players.

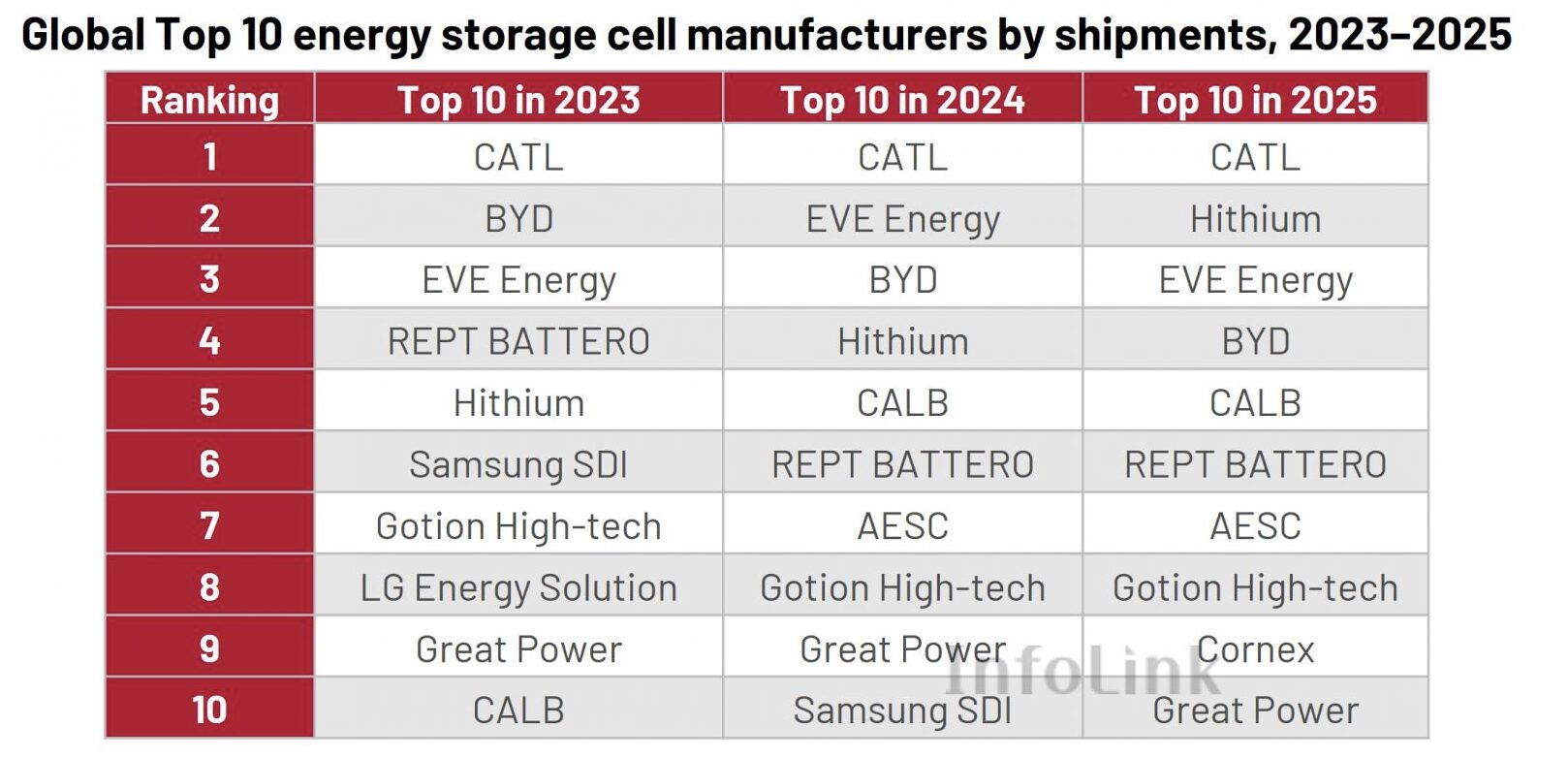

CATL, Hithium, EVE Energy, BYD, CALB and REPT BATTERO retained their positions as the top six suppliers globally, accounting for nearly 75 percent of total shipments. However, the overall competitive landscape remains fluid, with no clear long-term winner yet emerging.

Image credit: InfoLink

A key theme during the year was a rapid supply demand reversal. Between the second and third quarters of 2025, the market shifted from oversupply to a tight balance and subsequently entered a period of cell shortages. This transition triggered significant price volatility, as manufacturers moved from attempted price increases to resistance from downstream players before eventually passing higher costs through the value chain. System integrators responded by diversifying supply sources, contributing to ongoing quarter by quarter fluctuations.

Looking ahead, InfoLink expects the core positions of the top six suppliers to remain largely unchanged in 2026. At the same time, mid-tier players are likely to face increasing pressure as emerging manufacturers scale up and intensify competition for top ten rankings. Korean manufacturers may represent a key variable, supported by more favourable policy conditions that could gradually reshape the market structure.

The utility scale segment continued to dominate growth in 2025, with shipments reaching 556.74 GWh, up 96.73 percent year on year. The leading suppliers in this segment were CATL, Hithium, EVE Energy, CALB and BYD. InfoLink reports that production timelines for large format cells above 500 Ah are becoming clearer, with mass production expected to ramp up from late first quarter 2026 into the second quarter. Cell formats around 587 Ah and 588 Ah are emerging as the main direction for capacity expansion, with penetration of cells above 500 Ah expected to exceed 15 percent in 2026.

The small-scale storage market also showed resilience despite seasonal headwinds. Total shipments reached 55.65 GWh in 2025, reflecting growth of 75.54 percent year on year. Fourth quarter volumes increased compared with the previous quarter, defying the typical off-season slowdown. EVE Energy, REPT BATTERO and Great Power remained the top three suppliers. InfoLink highlights a gradual shift in residential storage from 100 Ah cells towards 314 Ah formats, which offer clearer cost advantages. Penetration of 314 Ah cells in this segment could approach 20 percent in 2026.

Geographically, shipments to markets outside China totalled 299.79 GWh in 2025, accounting for around 49 percent of global volumes. In the second half of the year, the non-China share rose to 51.3 percent, marking the first time shipments outside China exceeded those to the domestic Chinese market. The top suppliers to non-China markets were CATL, BYD, EVE Energy, CALB and Hithium. LG Energy Solution ranked ninth and was the only Korean manufacturer in the top ten. As new North American production capacity comes online, InfoLink expects Korean suppliers to gradually recover market share.

For 2026, InfoLink maintains its outlook for a tight supply demand balance in the first half of the year, followed by moderate easing in the second half. Based on manufacturer shipment plans and project progress across major regions, the firm projects global energy storage cell shipments to reach 801 GWh in 2026, with the market sustaining mid to high growth momentum.

The data presented by InfoLink is based on ongoing verification through interviews with upstream and downstream industry participants. Where companies did not provide official figures, estimates were derived from detailed market research. InfoLink notes that manufacturers official data should prevail in the event of any discrepancies.

Author: Bryan Groenendaal