x 90px (h)")

x 90px (h)")

x 90px (h)")

Subject: Biofuels

Cleaner fuel for aviation and road transport set for take-off.

The sands are shifting under the refining industry. Overcapacity and low utilisation rates will persist well beyond 2020 and, as we predicted, the shake-out of competitively weak refineries has begun. Could some of the old, marginalised units be useful tools in the energy transition, repurposed to produce low-carbon biofuels? I asked Alan Gelder, Head of Downstream Analysis, and Theo Zisis, Senior Analyst, Biofuels.

How much refining capacity needs to close?

A lot. We reckon 3.5 million b/d in the next three years across Asia, North America and Europe to get refining utilisation back up to the levels where the industry makes money. Four refineries have been axed so far this year – BP’s Kwinana (Australia, 146 kbd), Shell’s Convent (Louisiana, 260 kbd) and Tabangao (Philippines, 110 kbd), as well as Irving Oil’s Come By Chance (Newfoundland, 135 kbd) which was already offline. There will be more.

How do refiners weigh up closure versus repurposing?

Closure has always been a difficult decision for the company and the community around it – refineries are big employers. The energy transition might offer a new lease of life. It won’t work for all and depends on the circumstances of the individual refinery.

What is repurposing all about?

Refineries can be converted to produce biofuels, principally biodiesel, by shifting feedstock from crude oil to vegetable oils. Biodiesel has been around for more than a century and is compatible with standard diesel engines. But as a low-carbon fuel, its time has come. Processing vegetable oil yields light products, such as diesel and jet aviation fuel.

Is there much of a market for biodiesel?

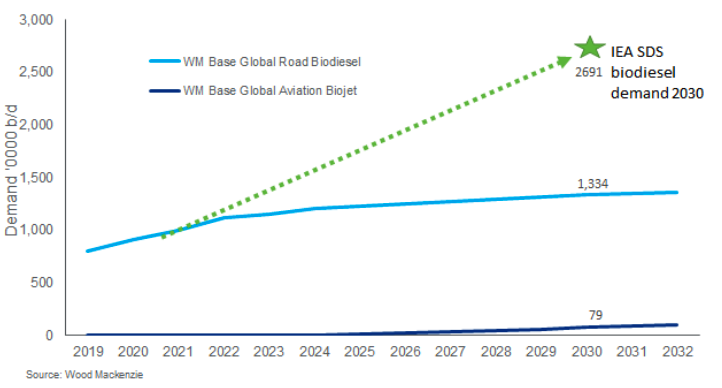

It’s small today at around 0.9 million b/d, meeting less than 1% of global oil demand and is used solely in road transport. But it’s going to grow faster than any other segment of oil demand, except perhaps petrochemicals. Our forecast is 1.5 million b/d by the 2030s, including up to 0.2 million in jet aviation. There’s potentially a lot of upside – the IEA Sustainable Demand Scenario (SDS) reckons we’ll need 3 million b/d by 2030 to get onto a 2oC or lower pathway. Getting to that level though requires a technology breakthrough, and soon.

All the major demand centres, among them India, need biodiesel, but the big growth market is California. There, low-carbon fuel standards are incentivising new investment in biodiesel capacity elsewhere in the US and in Singapore.

Biodiesel though can only ever be part of the decarbonisation solution for transport. Feedstock is a constraint. The global vegetable oil market is around 200 Mt a year, whereas road diesel and jet aviation fuel demand was around 1,200 Mt in 2019. But it’s readily blended with crude oil-based diesel or jet kerosene, helping to reduce emissions. The IEA SDS reckons bio-jet needs to be 10% of aviation fuel supply by 2030, a decade earlier than our base case forecasts, versus less than 1% today. As EVs come into the market, displacing light vehicles with ICE engines, blending rates can increase, sustaining demand for biodiesel.

Have many refineries have been repurposed?

Only Eni and Total have repurposed a refinery for biodiesel in the past, though ExxonMobil, Shell and BP produce biofuel alongside crude products in some refineries.

The first repurposing this downturn is Total’s Grandpuits (93 kbd) near Paris, at a cost of EUR0.5 billion. From 2024, Grandpuits will produce biodiesel, mainly for jet aviation, and bioplastics. The plant will also have plastics recycling and two photovoltaic solar plants. Grandpuits may be a template for others to follow – repurposed refineries of the future will be very different from the smoke-stack technology of last century.

Can you make money from biofuels?

Good question. Vegetable oil feedstock costs over US$100/bbl, whereas Brent crude is just over US$40/bbl – do the maths. Also, biodiesel units only produce the light end of the barrel and volumes are only about a quarter of those of the crude oil-based refinery they replace. They lose out on economies of scale.

So why are refiners so keen?

The strategy is long term. Biofuels are a bit like other early-stage zero-carbon technologiessuch as green hydrogen and carbon capture and storage – proven technically but not yet commercial. The money bit should come with investment, cost reduction and scale; but will also require supportive policy, including carbon pricing. The big R&D goal is to commercialise waste and residues, rather than food crops, as the feedstock, slashing costs and eliminating the threat of disruption to the food supply chain.

The Majors need to take risks to be leaders, investing in these emerging technologies as they are commercialised. Biofuels is one of them, a technology that can help both the refiner and its customers pursue their carbon-reduction goals.

Biodiesel has high growth potential through the transition as crude oil-based transport fuels face decline

Author: Simon Flowers

Simon is Chairman and Chief Analyst at Wood Mackenzie.

This article was originally published by Wood Mackenzie in their Get the Edge weekly feature and is republished with permission.

Disclaimer: The articles expressed in this publication are those of the authors. They do not purport to reflect the opinions or views of Green Building Africa, our staff or our advertisers. The designations employed in this publication and the presentation of material therein do not imply the expression of any opinion whatsoever on the part Green Building Africa concerning the legal status of any country, area or territory or of its authorities.