x90px (h)")

- Despite the ‘war on plastics’, demand over the coming decades will be robust, underpinned by the growing global middle-class and the material requirements of the energy transition.

- As an energy-intensive industry with carbon as a major feedstock, emissions in the chemicals and plastics sector will continue to grow at a rate that is at odds with Paris commitments without significant intervention, according to new research from Wood Mackenzie’s Cross-Polymer Demand Model.

Wood Mackenzie, a Verisk business (Nasdaq:VRSK), built two scenarios to see what polymer value chains might look like in 2-degree (Wood Mackenzie’s proprietary AET-2 scenario) and 1.5-degree (Wood Mackenzie’s proprietary AET-1.5 scenario) worlds. The base case scenario (Wood Mackenzie’s Energy Transition Outlook) reflects the company’s judgement of the most likely outcome, taking into account the expected evolution of policy and technology over the coming decades, and indicates the world is on a 2.8C-3C pathway warming trajectory.

As a subset of the industrial sector, the plastics value chain was responsible for 1.4 GtCO2eq in 2020, or 4% of energy-related emissions. In the base case, this nearly doubles to 2.6 BtCO2eq in 2040 and 7% of energy-related emissions. In a world in which more ambitious decarbonisation is achieved – such as WoodMac’s AET-1.5 scenario – this share could rise to one-third of total energy-related emissions, as other sectors aggressively decarbonise.

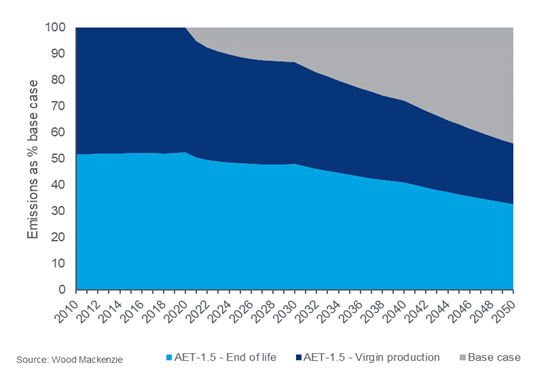

Wood Mackenzie AET-1.5 scenario emissions vs base case

Ashish Chitalia, Wood Mackenzie Head of Global Polyolefins, said: “As the world gears up for COP26 in Glasgow in November, countries around the world are announcing more stringent decarbonisation goals. While these are focused on country-level reductions, the impact of these objectives – if they are to be hit – will lie with industries operating in each territory.

“This will fall particularly hard on the plastics value chains, with carbon embedded in the product and integral to the production processes that create it. Our scenarios illustrate the size of the challenge facing the sector. If the industry does not address CO2 emissions, broader targets will be that much harder to hit, and we can expect the industry to be hit by the escalating cost of carbon.”

If the plastics value chain is to keep pace with other industries in efforts to decarbonise, Wood Mackenzie says that intervention must happen now.

Andrew Brown, Wood Mackenzie Senior Research Analyst, said: “Creating the most efficient plants and processes possible to maximise fuel efficiency, upgrading to latest generation technologies, and electrifying that which can be electrified can minimise carbon leakage. All three would drive out a reasonable proportion of net emissions in the production process.

“However, in isolation, they will not be enough. The industry will need to rapidly scale up its use of renewable carbon. While biopolymers and carbon capture, utilisation, and storage (CCUS) offer routes, the biggest and quickest way to build scale lies in ramping up the rate of recycling. As well as driving down emissions relative to virgin production, this route has the added advantage of dealing with the other major environmental challenge facing the industry: plastic waste.”

Even under Wood Mackenzie’s AET-1.5 scenario, polymer value chains would be producing 1.4Gt CO2-eq at a point when the world should be at net zero. This is the equivalent to the emissions of 350 coal-fired power plants or the carbon sequestered by a forest approximately three quarters the size of Brazil. While net zero implies that not all emissions will be displaced, it is likely under this scenario that more will be needed from the polymer value chain.

Brown added: “The most likely routes to achieving further decarbonisation would be through the adoption of more expensive renewable feedstocks – driving up costs for the industry – or in further demand reduction. Neither approach is likely to be palatable. Early action to scale and reduce the cost of carbon saving technologies is the best defence against these end points.”

Author: Bryan Groenendaal

Source: Woodmac