x 90px (h)")

x 90px (h)")

x 90px (h)")

- Decarbonising concrete – the pros and cons of the latest innovations

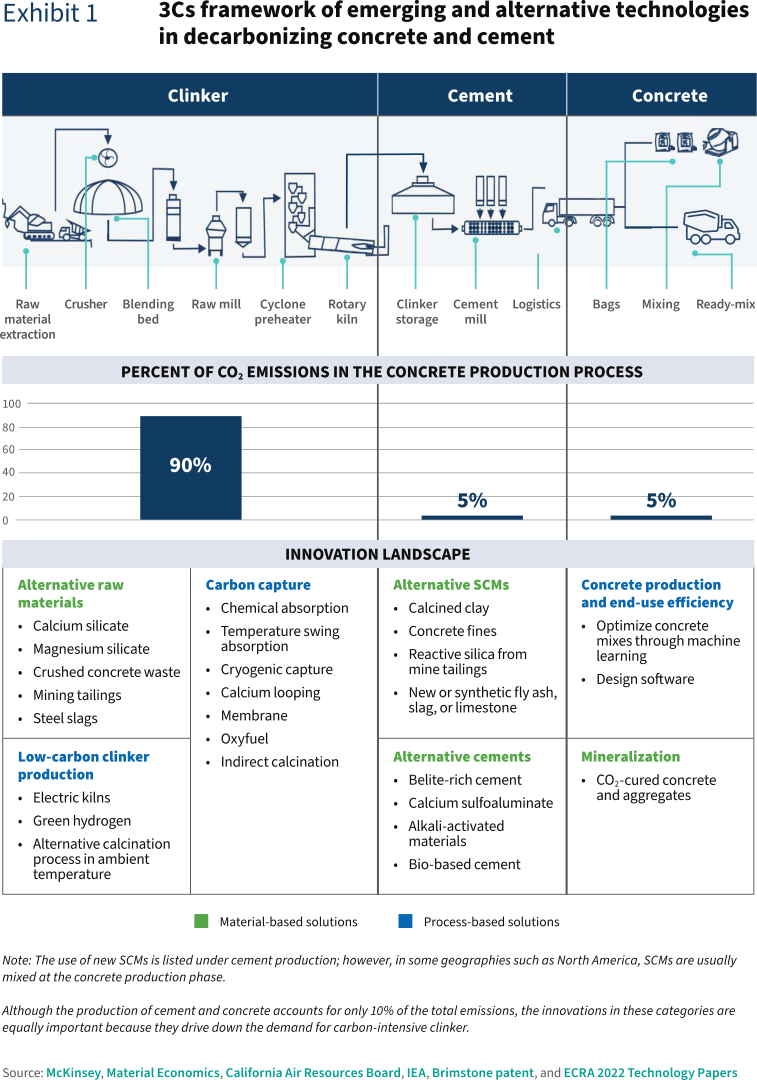

The concrete and cement industry currently accounts for 7-8% of global CO2 emissions, and the sectoral emissions will continue to increase if we keep making concrete the way it is produced today. The coming years will see significant growth in demand for concrete, particularly in the Global South, which means bringing many brand-new plants online. This provides a prime opportunity for investing in low- and zero-carbon concrete and cement production capacities to avoid locking in emissions for decades.

There is no silver bullet to decarbonize concrete and cement. On the one hand, the technologies that are readily available today, such as energy efficiency improvements, will not get us to net-zero by 2050. On the other, the most mature carbon capture technology today can achieve significant emission savings, but is expensive and energy intensive. Many policy-makers, investors, researchers, and industry stakeholders have expressed interest in understanding the new and emerging technologies that can accelerate the sectoral transition.

RMI’s insight brief The 3Cs of Innovation in Low-Carbon Concrete: Clinker, Cement, and Concrete provides a one-stop shop for understanding the landscape of emerging and alternative technologies to decarbonize concrete and cement. The insight brief details the pros and cons of each innovation and provides a technology’s applicability evaluation framework for assessing which of these technologies are most effective for their unique conditions.

Key takeaways of this insight brief on the deployment of innovative technologies include:

- Innovations are actively happening in each production phase of the concrete and cement value chain.

- There is no one-size-fits-all solution. It is important to evaluate the technology applicability at regional and plant levels.

- Using innovative low-carbon materials in nonstructural components is a relatively low-risk way to start market penetration.

- In this decisive decade, the cheapest and fastest options should be deployed first while we prepare the industry for carbon capture technology commercialization in the 2030s.

Download full report HERE

Authors: Zhinan Chen, Radhika Lalit

This article was originally published by the RMI and is republished with permission through the Creative Commons CC BY-SA 4.0 license.

Disclaimer: The articles expressed in this publication are those of the authors. They do not purport to reflect the opinions or views of Green Building Africa or our staff. The designations employed in this publication and the presentation of material therein do not imply the expression of any opinion whatsoever on the part Green Building Africa concerning the legal status of any country, area or territory or of its authorities.