- Global cumulative lithium-ion battery capacity could rise over five-fold to 5,500 gigawatt-hour (GWh) between 2021 and 2030, says Wood Mackenzie.

The Asia Pacific region, led by China, accounted for 90% of the world’s battery manufacturing in 2021. By the end of decade, the region is expected to reduce its share to 69%. While North America’s cell capacity could expand 10-fold by 2030, it still lags behind Europe which is on track to overtake North America in 2022 and will account for over 20% of global capacity by 2030 through more rapid expansion.

Wood Mackenzie consultant Jiayue Zheng said: “The electric vehicle (EV) market accounts for almost 80% of lithium-ion battery demand. High oil prices are supporting more markets to roll out zero-emission transportation policies, causing demand for lithium-ion battery to skyrocket and exceed 3,000 GWh by 2030.

“The lithium-ion battery market already encountered shortages last year due to thriving EV market demand and rising raw material prices. Under our base case scenario, we project that battery supply will not meet demand until 2023.”

Global battery manufacturers are responding with massive expansion plans, taking total capacity to more than 5,500 GWh by 2030 across 300 manufacturing facilities. Among them, Chinese manufacturers have announced plans to build more than 3,000 GWh of capacity to date.

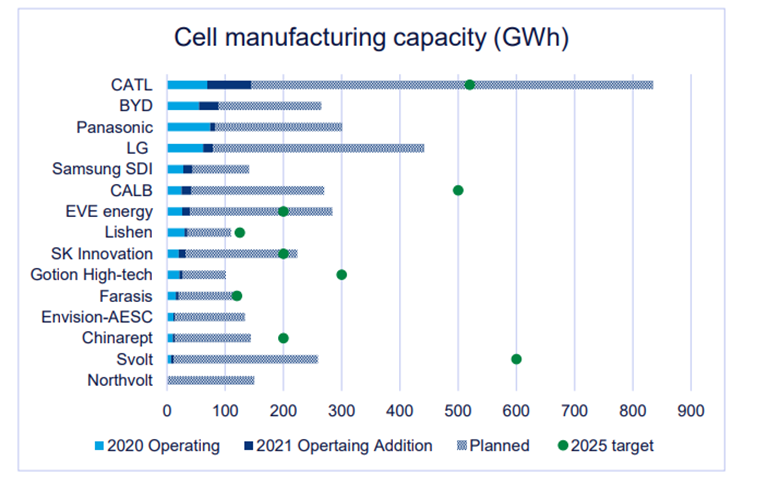

The top 15 manufacturers by planned capacity put into operation a total of about 200 GWh in 2021, and the cumulative capacity reached 600 GWh. Meanwhile, 3,000 GWh of capacity is at the planning or construction stage. CATL leads the expansion with outstanding operating and planned capacity – 800 GWh in total by 2030. Chinese battery manufacturers such as SVOLT, CALB and Gotion High-Tech also have ambitious 2025 capacity targets. Wood Mackenzie expects many more new plant announcements in 2022.

Battery manufacturing capacity by 15 global manufacturers (including JVs). Image credit: Woodmac

Another trend to watch is the growing prominence of lithium iron phosphate (LFP) batteries as nickel-cobalt-manganese (NCM) batteries lose market share. Historically, the EV and energy storage system markets have mostly deployed NCM batteries given their availability and maturity. In 2021, NCM still accounted for half of the market share. However, LFP batteries began tapping into the market with competitive cost, long lifecycle and high safety performance, making them an attractive option for both power and energy applications. Wood Mackenzie projects that LFP’s market share will surpass NCM in 2028.

Author: Bryan Groenendaal

Source: Woodmac