x 90px (h)")

x 90px (h)")

x 90px (h)")

Opinion

- Market reform is being paced to protect Eskom’s revenues rather than enable real competition.

- Transmission delays and grid constraints are being tolerated despite clear private sector solutions.

- Declining demand for coal based power is driving a controlled slowdown of decentralisation.

South Africa’s electricity reform is beginning to resemble an exercise in control rather than competition. While the publication of draft trading rules by the National Energy Regulator of South Africa signals progress on paper, the substance of the framework points to a far more cautious, and arguably deliberate, approach to change.

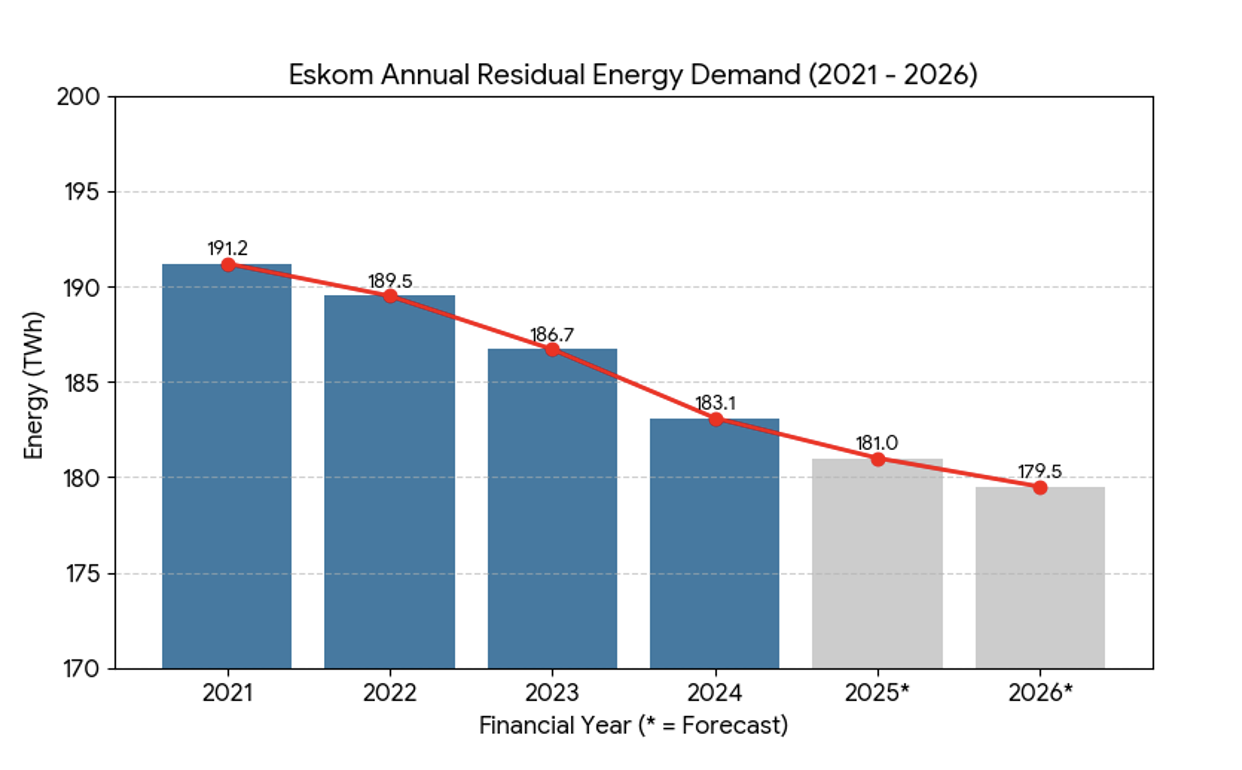

At the heart of the issue is a simple but uncomfortable reality. Demand for Eskom supplied electricity is falling. Data from the Eskom Data Portal shows a steady decline in sales from around 191 TWh in 2021 to approximately 179 to 180 TWh by 2026. This is not a cyclical dip. It reflects a sustained shift as commercial, industrial and residential users invest in solar PV, battery storage and other forms of self-generation.

Eskom data regularly compares “Residual Demand” (demand from the grid) against previous years, showing a consistent downward trend in peak and energy demand. Image credit : Eskom Data Portal

This erosion of demand strikes directly at Eskom’s revenue base, which remains heavily dependent on electricity sales from an ageing fleet of coal fired power stations. These assets are increasingly expensive to run, highly polluting and less competitive against rapidly falling renewable energy costs. As a result, any rapid move toward a fully liberalised market would accelerate Eskom’s financial decline. Read more

It is within this context that the current reform trajectory must be understood. The wholesale electricity market (SAWEM), long positioned as the cornerstone of a competitive power sector, continues to face delays in implementation. At the same time, the proposed bilateral trading rules introduce participation caps, phased access and structural limitations that restrict meaningful competition for years.

When it is eventually launched, and in line with the draft trading rules recently presented by the national energy regulator, NERSA, to the SAWEM Working Group, it is likely that only large users will be permitted to participate as contestable customers. Even then, procurement from third parties will be limited to 20% in the early years. The slow expansion of these limits over a six year horizon sends a clear signal. This is not a market being opened. It is a market being rationed.

Restrictions are set to extend beyond licensed traders to include independent power producers, aggregators and generators above 100 kW. In doing so, the framework compresses what should be a diverse and dynamic ecosystem into a tightly managed system where innovation is constrained and competition diluted.

Smaller scale distributed generation, particularly rooftop solar, is effectively excluded from meaningful participation. Systems that could contribute to grid resilience and reduce pressure on centralised generation are instead confined to self-consumption. At a time when South Africa is attempting to transition away from a coal heavy, air polluting energy mix, sidelining decentralised capacity appears less like oversight and more like intent.

Transmission infrastructure reinforces this pattern of delay. The establishment of the National Transmission Company of South Africa was widely welcomed as a structural reform. Yet progress in expanding the grid has been slow, despite estimates that more than 14000 km of new lines are required to unlock planned generation capacity.

Private sector participation in transmission, which could accelerate delivery and ease fiscal pressure, remains limited by policy uncertainty and procurement inertia. The consequence is a persistent grid bottleneck that prevents new renewable projects from connecting, effectively delaying investment without formally restricting it.

For investors in solar, wind and battery energy storage systems, the implications are increasingly clear. Opportunities exist, but they are being deferred. Projects that are technically and financially ready face extended timelines due to grid access constraints and uncertain market rules. Capital, in turn, becomes more cautious and more expensive.

At the same time, the structure of non-by-passable charges ensures that even where third party supply is permitted, the space for competition remains narrow. A significant portion of the electricity bill remains tied to legacy costs, network charges and regulated components payable to the incumbent. This limits the commercial incentive for customers to switch and reduces the impact of new entrants.

Overlaying these structural constraints is a growing concern around governance and enforcement. Allegations linked to projects under the Renewable Energy Independent Power Producer Procurement Programme highlight weaknesses in oversight during project execution. Questions around BBBEE compliance, localisation commitments and labour practices point to gaps that, if left unaddressed, risk undermining confidence in the broader transition. Read more

Even as policy and infrastructure challenges mount, Eskom’s environmental trajectory underscores the cost of delay. The utility remains one of the world’s largest emitters, and its emissions reduction strategy reflects the limits of incremental change. A proposed spend of around R46 billion delivers only a 7 to 8% reduction in sulphur dioxide emissions by 2031. This modest outcome is a direct consequence of a system that must continue relying on high emitting coal plants to maintain stability.

The government’s parallel push to tighten control over distributed generation adds another layer to the narrative. Mandatory registration of grid connected solar systems and the introduction of tariffs such as Homeflex signal an effort to retain visibility and revenue from a segment that is steadily moving beyond centralised supply. While grid management is a legitimate concern, the approach risks discouraging further adoption of clean energy solutions.

Taken together, these developments point to a transition that is being carefully managed to avoid destabilising Eskom, even if that means slowing the pace of reform. The decline in demand for Eskom’s electricity is not being met with accelerated market liberalisation, but with mechanisms that temper its impact.

This strategy may offer short term stability, but it comes at a cost. Delayed implementation of the wholesale market, constrained participation, slow transmission build out and weak enforcement collectively dampen the very competition needed to drive efficiency, lower costs and reduce emissions.

South Africa is not lacking in policy ambition or private sector interest. What is increasingly evident is a reluctance to move at the speed required. Until market access is genuinely opened and transmission infrastructure is expanded at scale, decentralisation will remain more promise than reality.

In the end, the risk is not that reform fails outright. It is that it succeeds too slowly, shaped less by the needs of the future and more by the constraints of the past.

Author: Bryan Groenendaal

Disclaimer: The articles and videos expressed in this publication are those of the authors. They do not purport to reflect the opinions or views of Green Building Africa, our staff or our advertisers. The designations employed in this publication and the presentation of material therein do not imply the expression of any opinion whatsoever on the part Green Building Africa concerning the legal status of any country, area or territory or of its authorities.